Money Market Update

www.concoda.com

Money Market Update

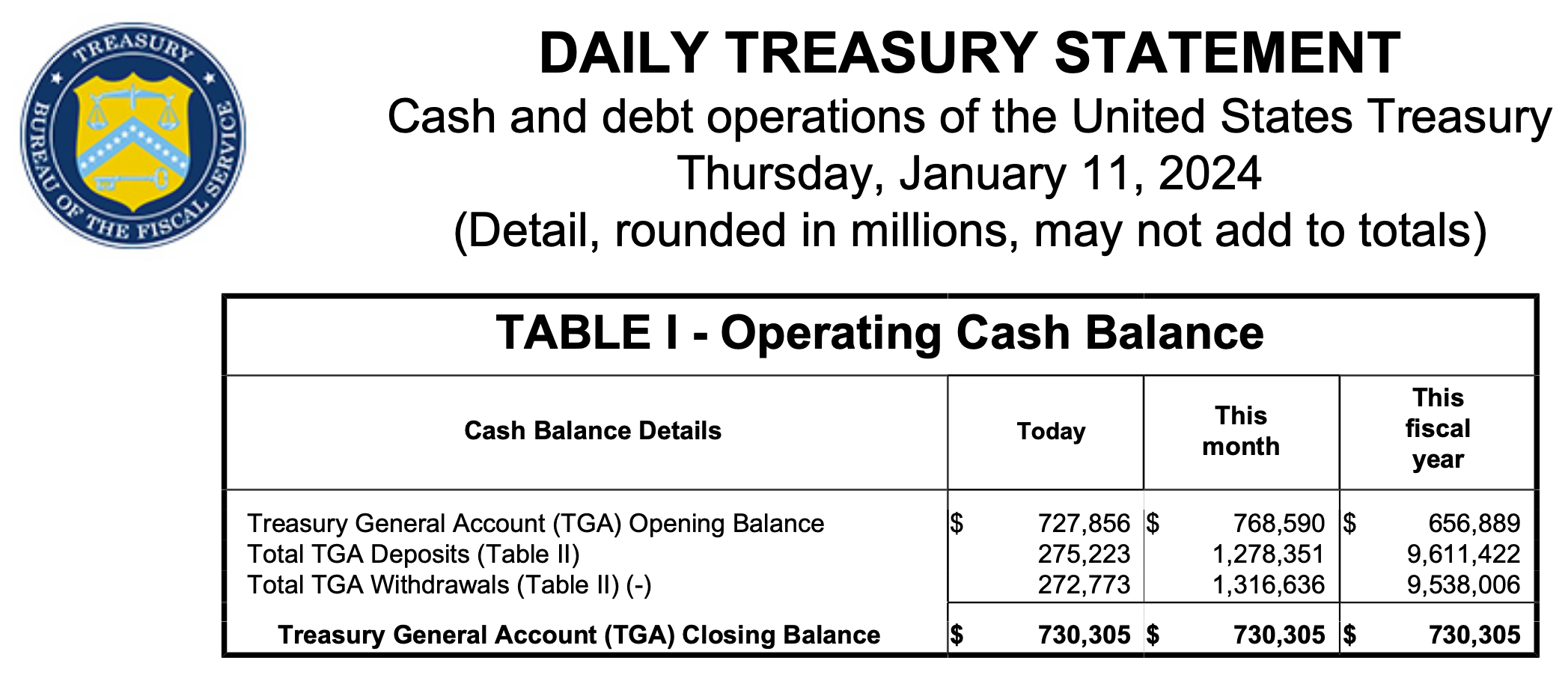

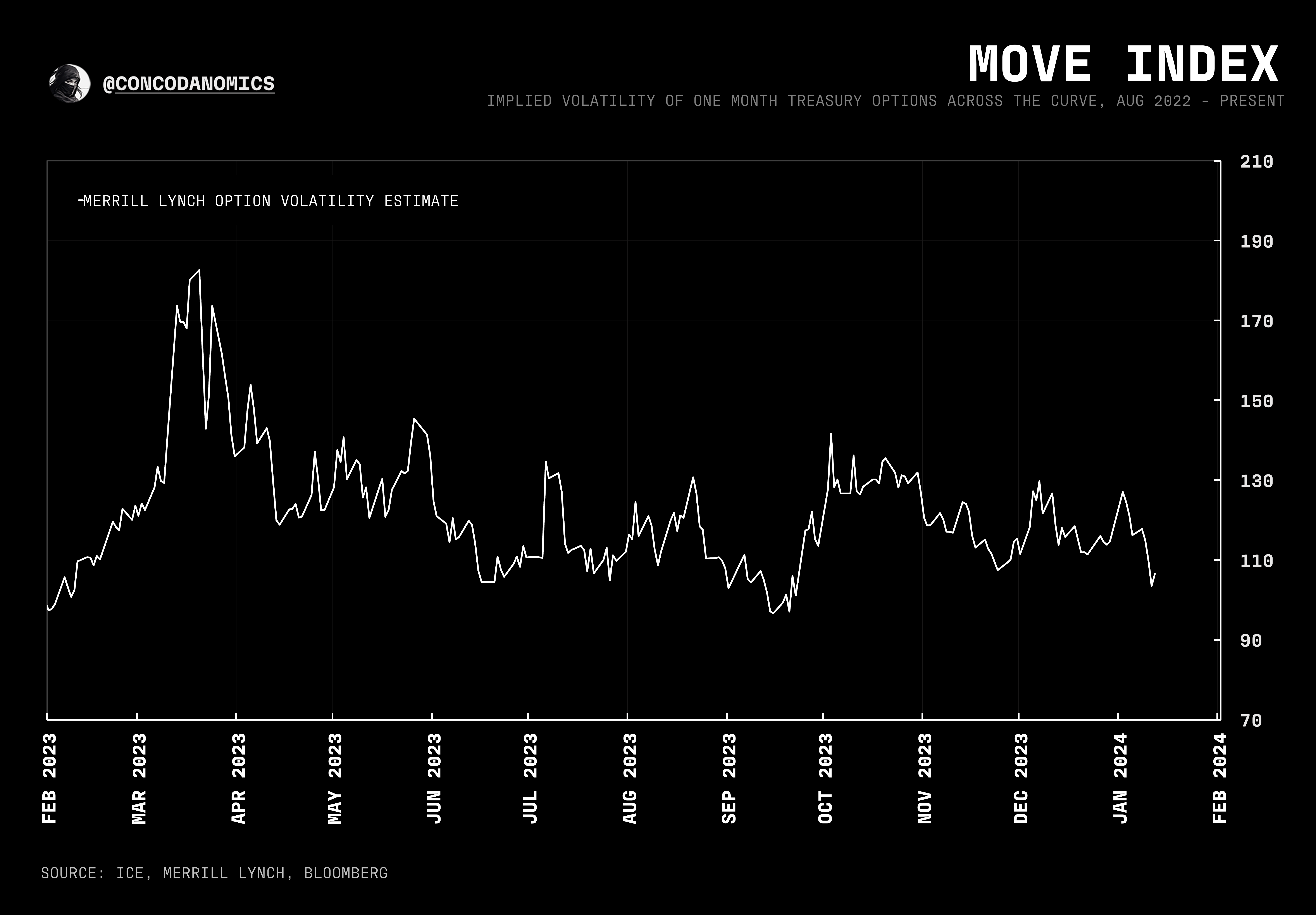

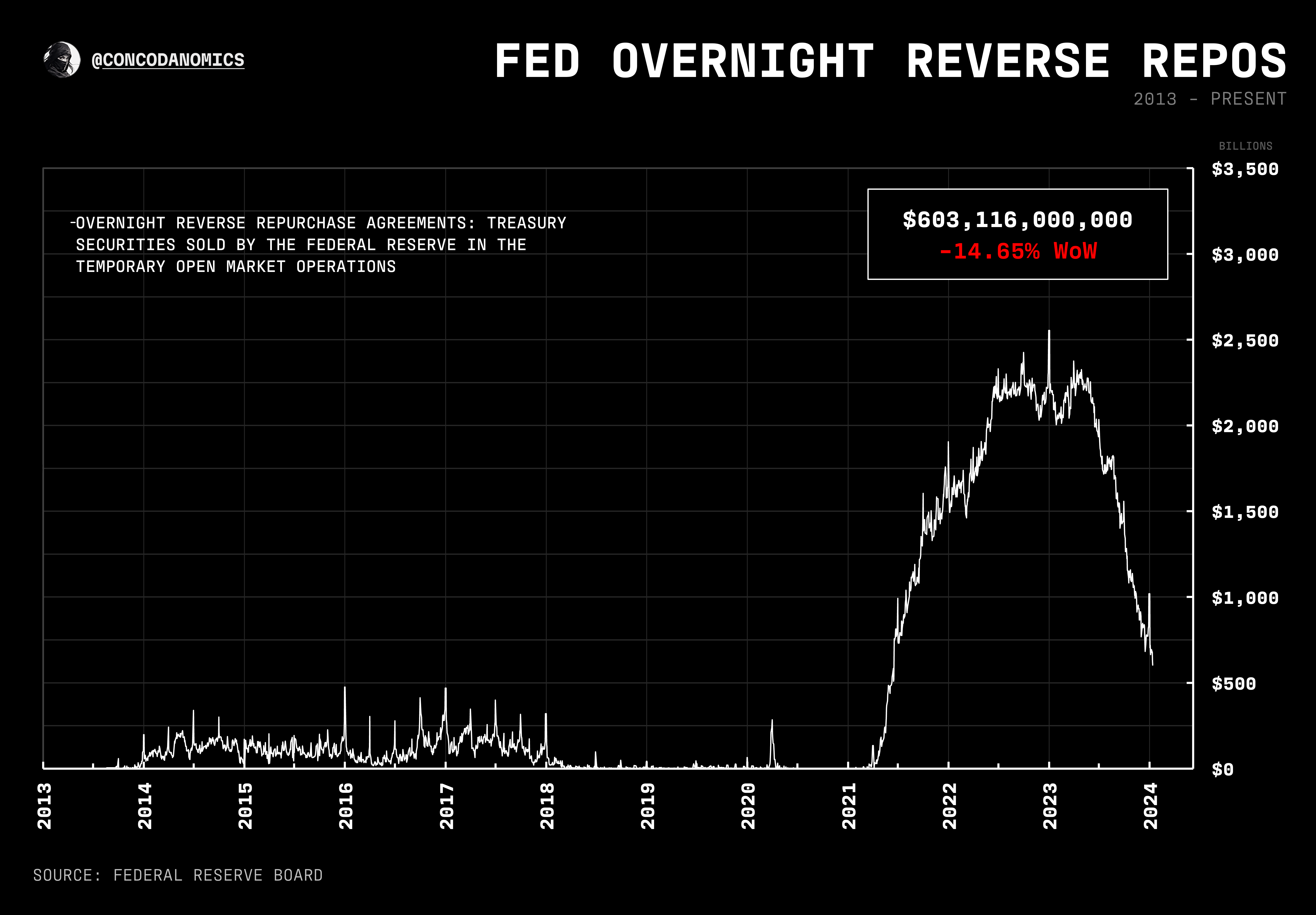

money markets return to normal after a rockier-than-usual year-end, with repo rates, fails, and treasury volatility falling. meanwhile, the Fed's RRP continues its descent to the zero bound

In case you missed it — or you’ve just joined us — our primer on the coming changes to the Treasury market went live recently (link below)…

In Demystifying the Repo Market Part One, we looked at triparty repo, the “base layer” of repo markets. Next, we’ll delve into the “upper layers”, the first being the dealer-to-dealer segment, showing how prominent players trade the most sophisticated market in the dollar funding ecosystem:

But first, a money market update…

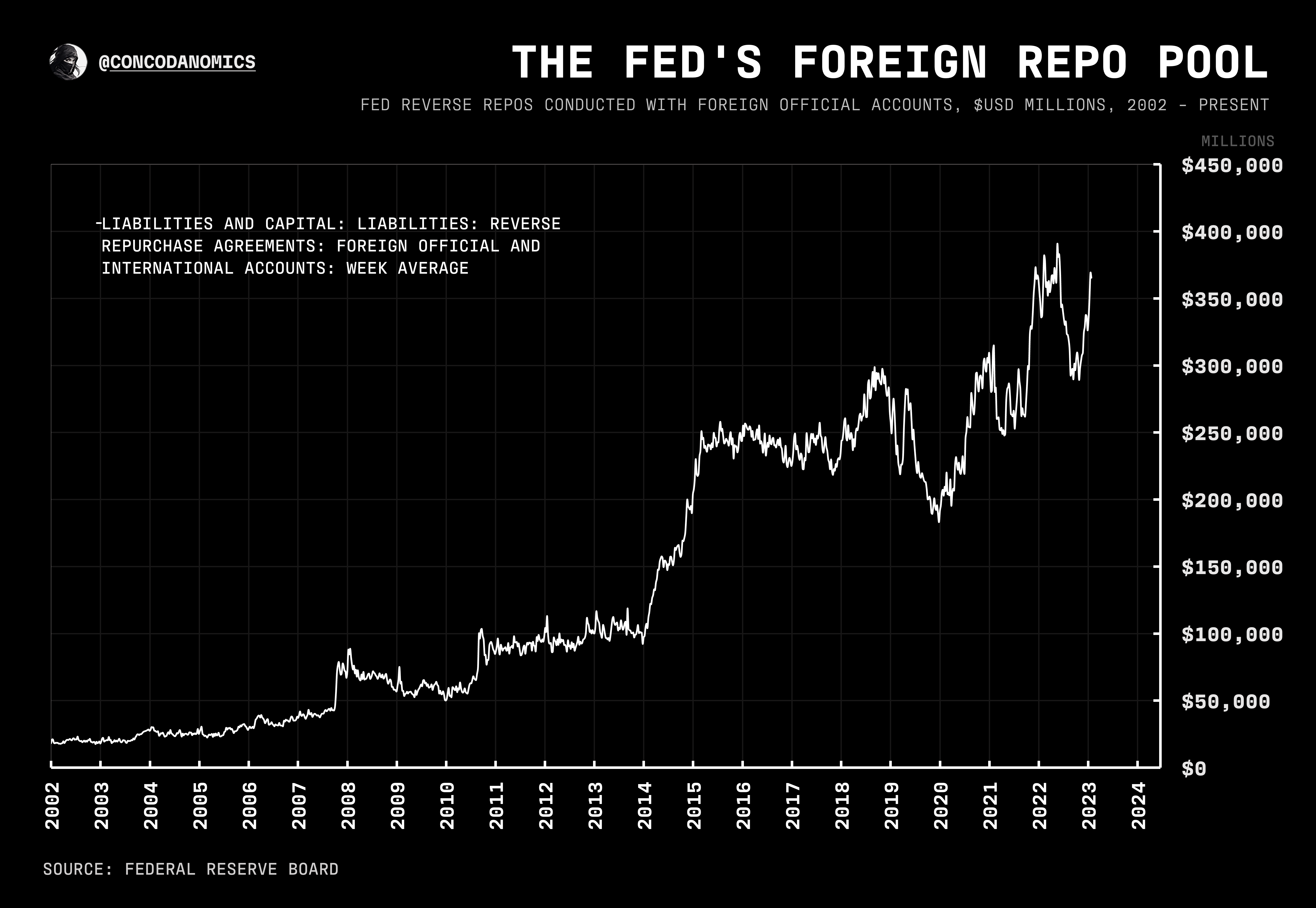

I have a question about the "jaws of the Fed" and how they compete with macroeconomic and fiscal forces. As I understand it, largely from your work (thank you), the Fed uses FIMA, RRP, FRP, etc. to set a lower bound for credit rates, and IORB for the upper bound.

Let us speculate that the Fed will use these facilities to cut rates by 100bp in 2024. On the fiscal side, however, Treasury is issuing literally trillions of dollars to finance public debt and deficits. Once-reliable foreign investors are drying up, and the hedge funds stepping in to soak up T-bills are demanding much higher rates, pushing the 10-year to 5.5%.

What happens to the cost of credit in the crosswinds? Which forces prevail?